3 Requirements to Qualify Your Home Office for a Tax Deduction Return to Articles

3 Requirements to Qualify Your Home Office for a Tax Deduction

Disclaimer: This blog may contain affiliate links .

Are you lucky enough to work from home? Only 38% of those surveyed by the Pew Research Center said that all, or most of their work responsibilities can be completed at home. Of that group, 54% would like to continue working from home if they had the choice. While seven out of ten work remotely, only 31% of those individuals are eligible for the home office deduction according to Andrew Keshner of MarketWatch.

The deduction, which is applicable to both homeowners and renters alike, can include property types such as mobile homes and boats, but not hotels or inns. The location of the office can be inside the home in a distinct room or space, in the corner of a room, or in a separate building on the property, such as a detached garage or garden studio shed.

Does Your Home Office Qualify?

Can you deduct your home office from your taxes? According to the IRS , there are three requirements needed to qualify. It is important to examine: 1. Your employee status, 2. Home office location and 3. Your principal place of business.

First, are you a W-2 employee, self-employed, or an independent contractor? If your primary source of income is as someone else’s employee, your home office cannot be deducted. But, if you have a side-hustle, your second job qualifies for the home office deduction.

Secondly, is the office space exclusive to only your job? An exclusive space means that you cannot use that space for anything other than your business. Something as simple as a corner of your bedroom that is established with a desk and is only dedicated to your business would qualify as exclusive. But, if your office is located at the dining room table, where you host family gatherings a few times a year, it no longer qualifies for the deduction.

Finally, does that exclusive space also serve as the principal place of business? If you have a physical location besides your home in which you work out of, then the amount of time spent at each place will determine if your home office qualifies. Your home would not be considered your principal place of business if you spend the majority of time at the other location. One exception to this rule is if you always use your home office space to meet with customers or clients. If you host occasional meetings at home, then it doesn’t qualify. If you are a contractor or a sales person and most of your work is completed at various locations or even in your car, but you use your home office exclusively for administrative or other management activities, then you can receive a tax deduction.

How Much Can You Deduct?

There are two calculation methods used to determine your home office expense deductions: the simplified and the actual expense methods.

The “Simplified Method” is to multiply the area of your office by $5 per square feet, the prescribed rate, with a maximum deduction amount of 300 sq ft, or a total of $1,500.

The “Actual Expense” method uses the percentage of your home that is dedicated to business use. Calculate your home’s total square feet and the total square feet of your office space to determine the percentage.

Next, decide if each expense is direct, indirect or unrelated. You can deduct 100% of your direct expenses for the office. For example, if you had a built-in desk or shelving installed, these expenses would qualify for the 100% deduction. If your expenses are tied to the enitre home or another part of your house, they are considered indirect, then you determine the percentage of the cost, which can be applied to your business. Indirect expenses can include: mortgage interest, insurance, utilities, repairs, maintenance, depreciation and rent. If you replaced your hot water heater, you can write a percentage of that repair off for your home office.

The amount of time you work in your office should also be considered. If you work year-round at home, you get to claim full deductions. If you only use your office part time, then you cannot claim 100% of your expenses. Say for example that you are a teacher, but you have a side business. You spend all of your time in your home office during the 3 summer months. In this scenario, you can only deduct 25% (3/12) of your annual expenses.

Record Keeping Requirements

According to the IRS, the responsibility to prove entries, deductions, and statements made on your tax returns is known as the burden of proof. You must be able to provide documentation, by having the information and receipts for all expenses. Keeping adequate records and documenting evidence to prove your expenses will support your tax claim. You do not have to use a particular method of record keeping, but you must keep records that provide the information necessary to determine your deductions for the business use of your home. You should keep canceled checks, receipts and other evidence of the expenses you paid. “To meet the adequate records requirement, you must maintain an account book, log, statement of expenses, trip sheet, or a similar record of other documentary evidence that is sufficient to establish business/investment use.”

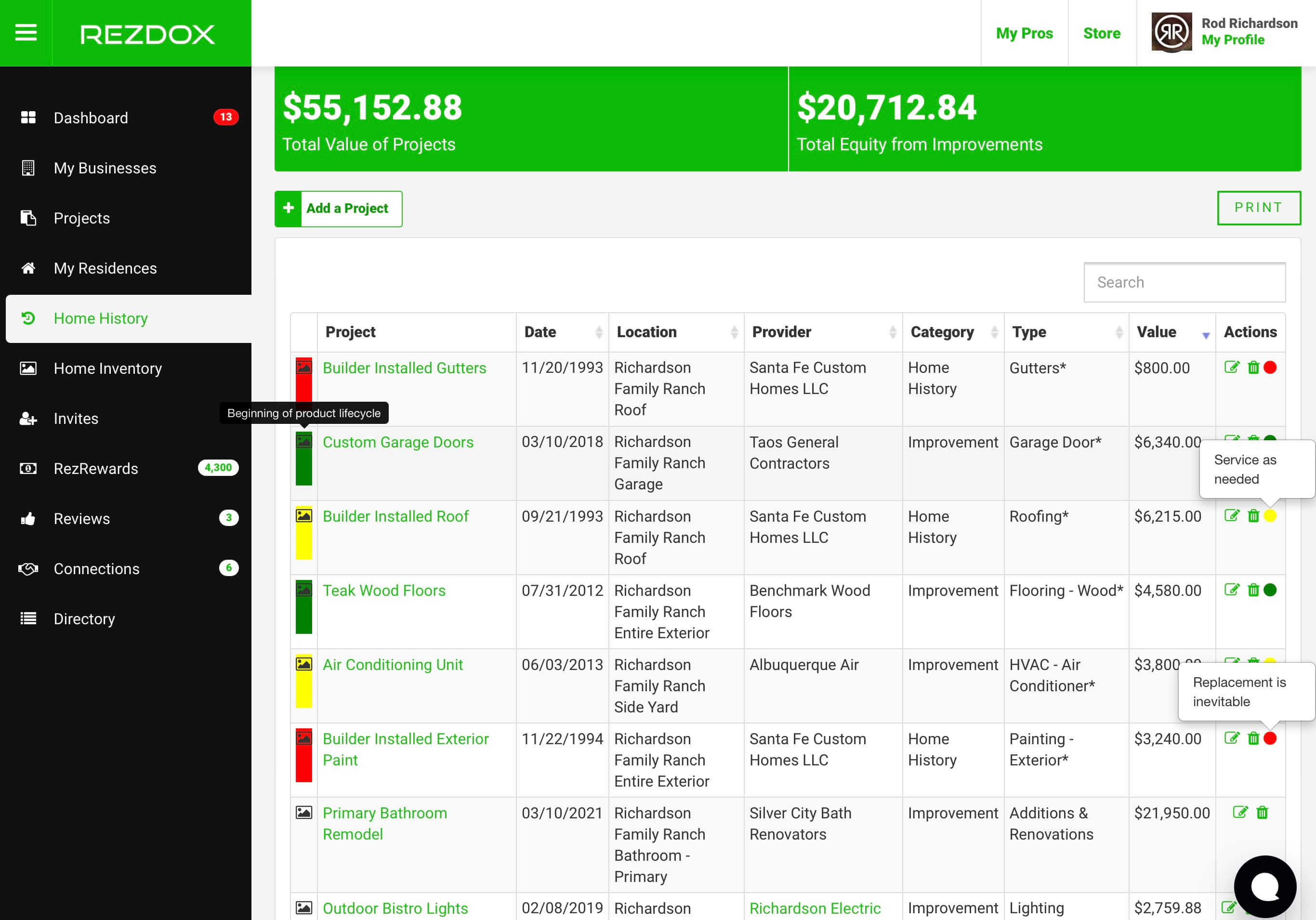

RezDox can help with record keeping by managing your home's repairs and improvements. You can easily determine direct vs. indirect home expenses when you enter a project into your Home History log and designate your home office as the project location. Your uploaded receipts, photos and invoices digitally stored and easy to find. If you are overwhelmed with receipts, let us help you digitize your records and create a home history report.

Trachelle Spencer

Co-founder | CEO RezDox

You may also like:

HOME REPAIRS vs. IMPROVEMENTS: To Claim or Not to Claim, That is the Question

Introducing RezDox RULS (Residential Useful Life Score)